It should be viewed in conjunction with other financial metrics like cash flow, liquidity ratios, and profitability measures. This holistic approach ensures a more balanced understanding of a company’s financial health. Determine whether your cash flow management policies and financing allow your company to pursue growth opportunities when justified. Over time, your business can respond to new business opportunities and changing economic conditions. Improve cash flow management and forecast your business financing needs to achieve the optimal accounts payable turnover ratio.

Delivering business outcomes

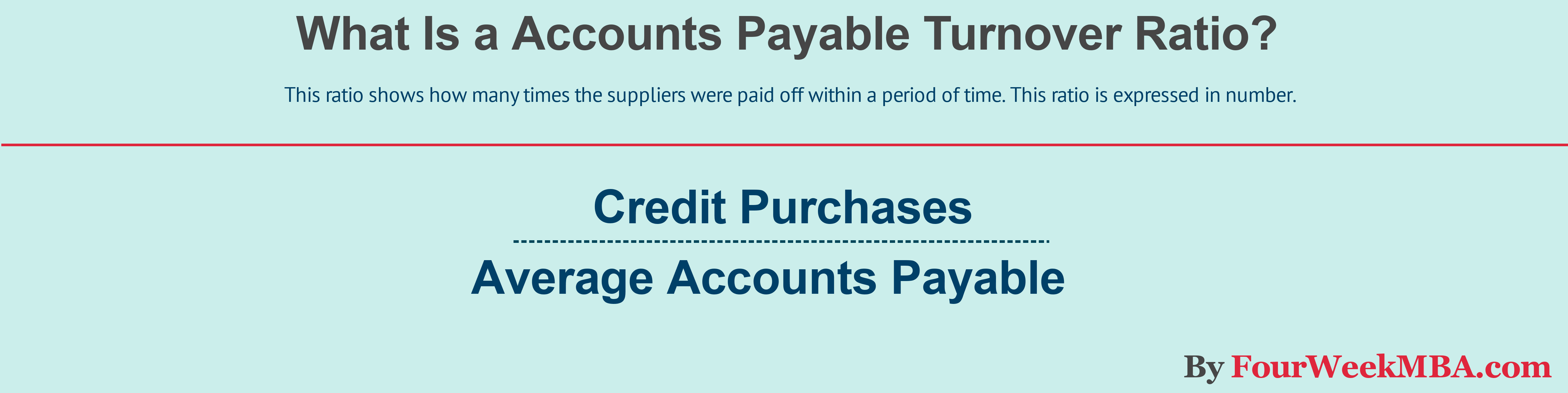

So, while the accounts receivable turnover ratio shows how quickly a company gets paid by its customers, the accounts payable turnover ratio shows how quickly the company pays its suppliers. The accounts payable turnover ratio shows investors how many times per period a company pays its accounts payable. In other words, the ratio measures the speed at which a company pays its suppliers. Both ratios provide valuable insights into a company’s financial health and, when used together, offer a more comprehensive view.

AccountingTools

However, it’s important to consider this in the context of the company’s overall financial strategy to ensure a balanced approach. Businesses with a higher ratio for AP turnover have sufficient cash flow and working capital liquidity to pay their suppliers reasonably on time. They can take advantage of early payment discounts offered by their vendors when there’s a cost-benefit. For example, an ideal ratio for the retail industry would be very different from that of a service business.

Business is Our Business

The total purchases number is usually not readily available on any general purpose financial statement. Instead, total purchases will have to be calculated by adding the ending inventory to the cost of goods sold and subtracting the beginning inventory. Most companies will have a record of supplier purchases, so this calculation may not need to be made.

Even before you receive a formal invoice, your AP department might accrue that expense since it’s a recurring expense they know is coming. You can use this accrual report alongside your recurring invoice report (see below) to help ensure all recurring expenses are accounted for. An accrued expense is an expense your business has incurred but hasn’t yet paid.

History of payments report

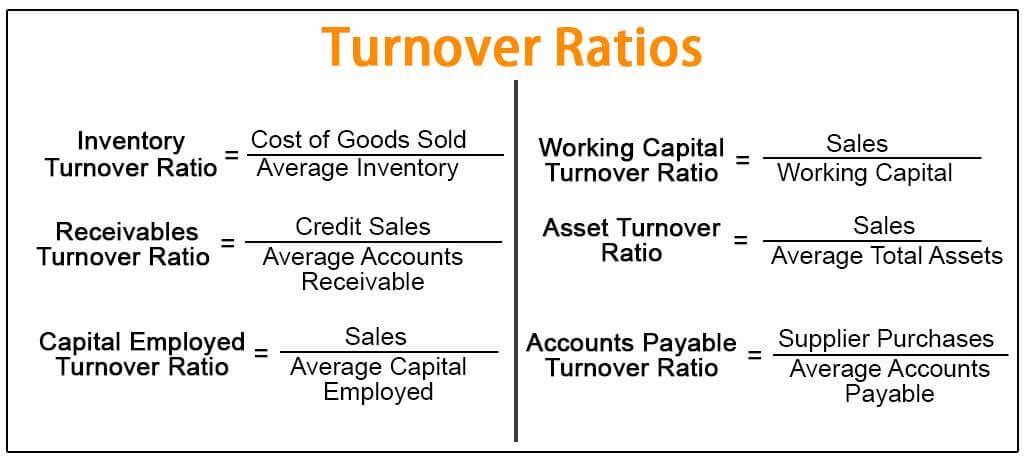

AP turnover shows how often a business pays off its accounts within a certain time period. Accounts receivable turnover ratio shows how often a company gets paid by its customers. The AP turnover ratio provides valuable insights into a company’s payment management efficiency and financial health. It provides insights into liquidity, working capital management, and the company’s ability to meet its financial obligations. Accounts payable turnover ratio, or AP turnover ratio, is a measure of how many times a company pays off AP during a period.

Having a high AP turnover ratio is important in determining the effectiveness of your accounts payable management. It can show cash is being used efficiently, favourable payment terms, and a sign of creditworthiness. The accounts payable (AP) turnover ratio gives you valuable insight into the financial condition of your company. It is used to assess the effectiveness what is a sales invoice complete guide on how to create one of your AP process and can alert you to changes needed in your financial management. As with all ratios, the accounts payable turnover is specific to different industries. The Accounts Payable Turnover is a working capital ratio used to measure how often a company repays creditors such as suppliers on average to fulfill its outstanding payment obligations.

- Another industry that can benefit from a high Accounts Payable Turnover Ratio is the healthcare industry.

- Automated AP systems can streamline invoice processing, reduce errors, and provide real-time visibility into payment status.

- An audit report is a document generated by your auditors that reviews your company’s financial records.

- Plan to pay your suppliers offering credit terms with lucrative early payment discounts first.

- However, an increasing ratio over a long period of time could also indicate that the company is not reinvesting money back into its business.

This can indicate that the company is managing its debts and cash flow effectively. Faster invoice processing means that payments can be processed more quickly, directly influencing the AP turnover ratio by potentially increasing it. This speed not only improves efficiency but also enhances supplier relationships through timely payments. On the other hand, a low AP turnover ratio can raise concerns about a company’s financial management. It may signal cash flow problems, indicating that the company is not efficiently settling its payables. Additionally, a low ratio might suggest that the company is missing out on early payment discounts, which could lead to higher operational costs.

The accounts payable turnover in days is also known as days payable outstanding (DPO). It’s a different view of the accounts payable turnover ratio formula, based on the average number of days in the turnover period. The DPO formula is calculated as the number of days in the measured period divided by the AP turnover ratio. A higher accounts payable turnover ratio is almost always better than a low ratio.

Your company’s accounts payable turnover ratio (and days payable outstanding) may be considered a higher ratio or lower ratio in relation to other companies. To balance cash inflows and outflows, compare your accounts payable turnover ratio with your accounts receivable turnover ratio. Or apply the calculation comparing the payables turnover in days to the receivables turnover in days if that’s easier for you to understand. Improve your accounts payable turnover ratio in days (DPO) by lowering the days payable outstanding to the optimal number that meets your business goals.